Withholding tax imposed on overseas property owners

For rent property

If you are a non-Japanese resident who owns an investment property in Japan, withholding tax as detailed below will be imposed.

In this case, the Lessee, a corporate, is responsible for this tax payment. Each month, a corporate tenant pays 20.42% of the monthly rent to the Japanese National Tax Office, and the remaining approx. 80% will be paid to the Lessor. But it doesn’t mean you will lose a 20.42% of your rent. If the paid withholding tax is exceeded from what you are supposed to pay, the excess tax amount will be refunded when you file the income tax every year in March in Japan.

If a Lessee is an individual tenant, there will be no such a tax liability. Only if a Lessor is overseas resident, and a Lessee is a corporate, then this tax will be applicable. But more importantly, it might affect your risks of the occupancy rate. It doesn’t matter if it is a large or small, most corporations are not willing to take such a tax payment liability, with the monthly payment burden. In this case, it makes it more difficult for overseas investors to find a corporate Lessee who could be relatively paying stable rent rather than those individual tenants.

But please don’t give up on investing in properties in Japan. There is always a solution. You can ask a property management company to master lease (ML) your property for this tax purpose. If both Lessor and Lessee is a corporate, the corporate Lessor will have an obligation to pay the withholding tax 20.42% every month. As a result, it doesn’t create any liability or extra payment work to the corporate tenant. Your property manager will pay the withholding tax 20.42% of the rent every month, and the remaining amount will be wired to your bank account. With this strategy, you will not lose your occupancy rate, but maximize the opportunity of the leasing activity.

When you are non-Japanese resident but buying a property in Japan, it is better to work with property management companies that provide such an ML solution.

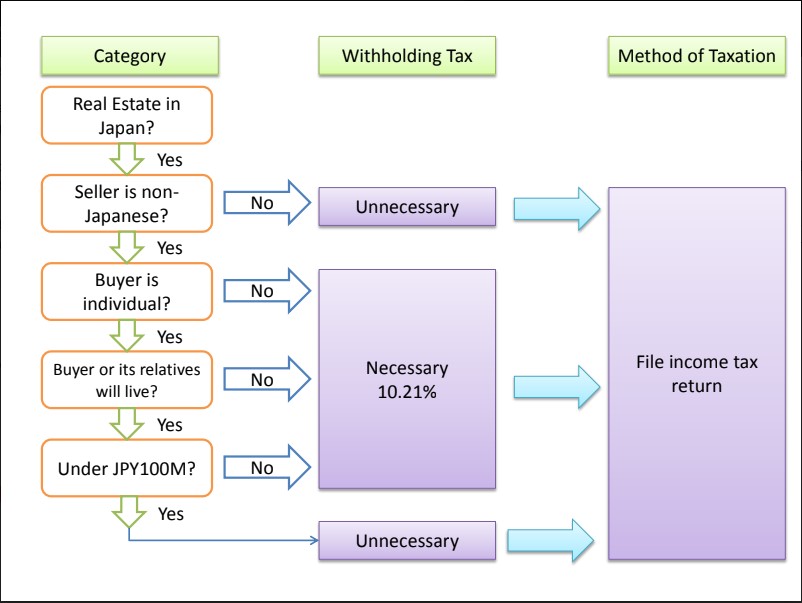

For sale of the property

There will be another withholding tax imposed when you sell a property in Japan as a non-Japanese resident. Please look at the flow-chart below.

As with a renting property, if a seller is a non-Japanese resident, and the property being sold is not for personal use, a buyer will have a liability to pay the withholding tax rate at 10.21%. Also, the same tax rate applies as withholding tax for rental income, the only remaining amount will be paid to the seller, but any excess of the paid tax amount will be refunded when a seller files the income tax in Japan. Unlike the rental income, it doesn’t prevent the buyer from purchasing a property from a non-Japanese resident, because the sales transaction is a one-off deal, so the tax payment will not continue on a monthly basis.

This withholding tax policy is designed to collect an accurate tax amount from overseas residents. It doesn’t matter whether a property owner is Japanese or non-Japanese, but anyone who lives outside of Japan has to follow these tax rules.

Written by Tsuyoshi Hikichi

AZUKI PARTNERS will provide tax consulting as well. For further questions or inquiry of advice, please feel free to contact us from HERE

For real estate advice please press HERE